How Canadian Experience Class income boost impacts finances

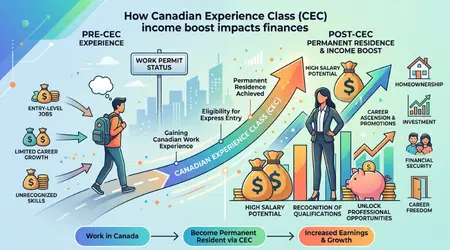

Transitioning from a temporary work permit to Permanent Residency (PR) in Canada is a significant milestone that often alters a household’s financial trajectory.

After years of living under the constraints of temporary status in cities like Toronto or Vancouver, many residents find that achieving PR through the Canadian Experience Class income boost impacts finances in ways that go far beyond a simple change in legal standing.

This transition marks the end of a “survival budget” phase and the beginning of long-term integration into the Canadian economy.

Key Insights for Your Financial Transition

- The Post-PR Salary Shift: Understanding how local experience and stable status influence compensation.

- Credit Accessibility: Changes in interest rates and borrowing limits following status updates.

- Tax Planning Requirements: Moving from basic tax filing to utilizing federal investment instruments.

- Asset Accumulation: Shifting focus from international remittances to building domestic equity.

Does Permanent Residency Increase Earning Potential?

Data regarding the Canadian labor market suggests a correlation between permanent status and increased earnings.

When analyzing how the Canadian Experience Class income boost impacts finances, it is important to note the removal of what is often termed a “risk discount.”

Employers may be hesitant to invest in extensive leadership training or high-level promotions for staff on permits with fixed expiry dates.

Upon receiving PR, the power dynamic in salary negotiations often shifts. Workers are no longer viewed as temporary contributors but as long-term organizational assets.

This change in status can lead to salary corrections as individuals become eligible for roles requiring high-level security clearances or long-term project oversight.

In many professional sectors, this transition facilitates a move into senior positions that offer more competitive compensation packages and improved contract stability.

How Permanent Status Changes Monthly Cash Flow

A primary way the Canadian Experience Class income boost impacts finances is through the transformation of an individual’s relationship with Canadian financial institutions.

Holders of temporary work permits may face higher scrutiny from lenders, which often results in restricted credit limits or higher interest rates on personal loans and vehicle leases.

Once an individual updates their status with their bank, they typically gain access to “Prime” lending rates.

This means that even if a gross salary remains constant, disposable income can increase because the cost of carrying debt decreases.

Lowering the interest paid on existing liabilities is a practical method of improving monthly cash flow without requiring an immediate raise from an employer.

++ How Canada student pathway ROI drives global study decisions

Case Study: Financial Progression in Ontario

Consider the typical progression of a tech professional in the Greater Toronto Area.

While on a post-graduation work permit, an individual might focus exclusively on liquid savings and remittances, often avoiding long-term Canadian investments like an RRSP due to uncertainty regarding their future in the country.

After securing PR via the CEC, a professional might see a salary increase that reflects their established Canadian work history.

For example, a jump in annual earnings from $75,000 to $98,000 significantly alters the monthly net take-home pay.

By redirecting this surplus into a First Home Savings Account (FHSA), the individual begins to build a down payment in a tax-advantaged environment.

This illustrates the compounding effect of legal stability on personal wealth.

| Feature | Temporary Resident (Work Permit) | Permanent Resident (CEC) |

| Average Loan Interest | Prime + 3-5% (Risk-based) | Prime + 0-2% (Standard) |

| Investment Access | Limited/Short-term focus | Full access to FHSA, RRSP, TFSA |

| Job Mobility | Restricted by permit conditions | Market-wide flexibility |

| Social Benefits | Basic healthcare coverage | Access to CCB and various grants |

Managing “Tax Bracket Creep” After an Income Raise

A significant increase in earnings often moves a taxpayer into a higher federal and provincial tax bracket.

In Canada’s progressive tax system, this means a portion of the new income is taxed at a higher percentage.

Understanding how the Canadian Experience Class income boost impacts finances requires a proactive approach to tax planning to ensure that raises result in actual wealth accumulation rather than just higher tax liabilities.

Registered Retirement Savings Plan (RRSP) contributions are a primary tool for managing taxable income.

By contributing to an RRSP, a resident can reduce their total taxable income, potentially dropping back into a lower bracket and triggering a tax refund.

For those newly endowed with PR status, automating these contributions ensures that the “lifestyle creep” associated with a higher salary does not come at the expense of long-term tax efficiency.

The Value of Local Experience Over Foreign Credentials

The Canadian labor market places a high premium on “Canadian experience,” which involves familiarity with local workplace culture, regulatory standards, and communication norms.

The CEC stream is designed to recognize this value. As a permanent resident with local history, an individual’s professional profile often shifts from “applicant” to “target” for recruiters.

This shift allows workers to negotiate for more than just a base salary.

Total compensation packages for permanent residents often include better health benefits, increased vacation time, and performance bonuses that are not always available to temporary staff.

This long-term career stability is a fundamental pillar of financial security in Canada.

Also read: Why Canadians Are Feeling More Financially Confident — Even Amid Economic Anxiety

Real Estate Considerations Following PR Acquisition

While PR status simplifies the mortgage application process and may exempt buyers from certain non-resident taxes, homeownership involves significant costs beyond the mortgage payment.

Property taxes, maintenance, and insurance must be factored into the new household budget.

It is often recommended to use the first year of permanent residency to strengthen a Canadian credit score.

A higher income combined with a “thick” credit file meaning a long history of diverse, well-managed accounts allows for better negotiation with mortgage brokers.

This preparation ensures that the transition to homeownership is sustainable and does not overextend the household’s new financial capacity.

Strategic Planning for Future Stability

The transition through the Canadian Experience Class is a long-term process.

The financial advantages of PR are substantial, but they require a strategic shift from immediate survival to long-term stewardship of resources.

By focusing on tax efficiency, credit optimization, and domestic investment, new permanent residents can turn their initial income gains into a lasting foundation for their future in Canada.

Careful management of these new opportunities ensures that the benefits of permanent status are maximized for years to come.

Common Questions Regarding Post-PR Financial Life

Does my credit score reset when I receive PR?

No, your credit history remains attached to your name and Social Insurance Number (SIN).

However, notifying your creditors of your change in status can improve your internal risk rating at the bank, often leading to immediate offers for lower-interest products or higher credit limits.

Can I continue to send money abroad with a higher income?

Yes, though many financial planners suggest reviewing the ratio of remittances to local savings. Building a solid financial base in Canada provides the security necessary to continue supporting family abroad over the long term.

Am I eligible for more government benefits now?

Permanent residents have full access to social programs, including the Canada Child Benefit (CCB) and various provincial education grants.

zzThese benefits act as an indirect income boost, providing additional support for families that may not have been fully accessible under a work permit.